QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

隨著2018年第二個考試窗口的關(guān)閉,很多學(xué)員已經(jīng)開始準(zhǔn)備第三個考試窗口的考試了。

為了讓大家更好的掌握AICPA官網(wǎng)推出的7月份考綱更新,小編特意為大家詳細列舉了每科的考試變化更新內(nèi)容。

考綱具體變化內(nèi)容在《Uniform CPA Examination BLUEPRINTS(Effective Date July.1,2018)》和《Summary of revisions to the Uniform CPA Examination Blueprints(Effective Date July.1,2018)》中有詳細介紹

今天先為大家整理了AUD科目的更新內(nèi)容。滿滿干貨,往下翻~!

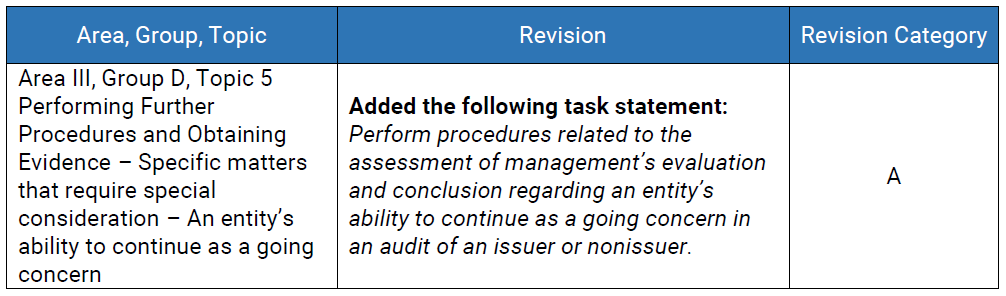

1.Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern

考綱變化:反映SAS No.132(AU-C 570 The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern):在Performing Further Procedures and Obtaining Evidence階段,增加Specific matters that require special consideration–An entity’s ability to continue as a going concern;

考綱解讀:相當(dāng)于考試對going concern問題增加了一個考點,以前愛考針對going concern發(fā)表不同意見,現(xiàn)在多了一個考點——審計師對企業(yè)的going concern進行測試和評估

補充學(xué)習(xí):The objectives of the auditor are as follows:

To obtain sufficient appropriate audit evidence regarding,and to

conclude on,the appropriateness of management's use of the going

concern basis of accounting,when relevant,in the preparation

of the financial statements

?To conclude,based on the audit evidence obtained,whether substantial

doubt about an entity's ability to continue as a going concern

for a reasonable period of time exists

?To *uate the possible financial statement effects,including the

adequacy of disclosure regarding the entity's ability to continue

as a going concern for a reasonable period of time

?To report in accordance with this section

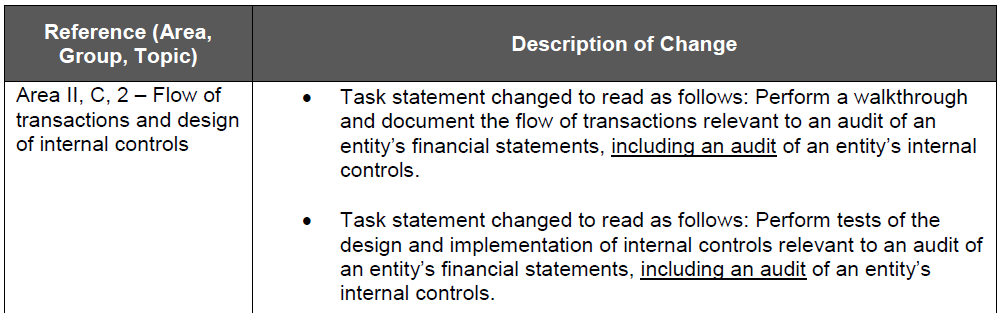

2.Audit of Internal Control Over Financial Reporting

考綱變化:反映SAS No.130(AU-C 940 An Audit of Internal Control Over Financial Reporting[ICFR]That Is Integrated With an Audit of Financial Statements)的術(shù)語變化,將“an examination of entity's internal controls"統(tǒng)一改成”An audit of entity's internal controls"

考綱解讀:此點變更僅是術(shù)語變化,為了對財務(wù)報表內(nèi)部控制的審計,與財務(wù)報表審計能更好地結(jié)合,考試基本不會受到影響。

3.New Reporting Standards Issued by PCAOB

官方通知(非考綱變化):會對PCAOB發(fā)布的new reporting standards進行考核,具體時間是除了Critical Audit Matters(CAM)的其他內(nèi)容從2018年7月以后考核,CAM相關(guān)內(nèi)容從2019年7月以后考核。

解讀:學(xué)員應(yīng)當(dāng)加強這部分針對上市公司審計報告準(zhǔn)則的學(xué)習(xí),但是今年的考綱暫時沒有涉及這里,推測今年下半年考試碰到的幾率不大,會是明年審計考試的“重頭戲”。

?補充學(xué)習(xí):critical audit matters

?Relates to accounts or disclosures that are material to the financial statements,and Involved especially challenging,subjective,or complex auditor judgment

?Factors the auditor should take into account in determining CAMs:

a.The auditor's assessment of the risks of material misstatement,including significant risks;

b.The degree of auditor judgment related to areas in the financial statements that involved the application of significant judgment or estimation by management,including estimates with significant measurement uncertainty;

c.The nature and timing of significant unusual transactions and the extent of audit effort and judgment related to these transactions;

d.The degree of auditor subjectivity in applying audit procedures to address the matter or in *uating the results of those procedures;

e.The nature and extent of audit effort required to address the matter,including the extent of specialized skill or knowledge needed or the nature of consultations outside the engagement team regarding the matter;

f.The nature of audit evidence obtained regarding the matter.

填寫下面表單,領(lǐng)取2018年AICPA大禮包一份!